When I set out to write a newsletter about the tech industry in Asia, I first wanted to write about “Super Apps”.

To confidently write this post, I needed to spend time studying existing super apps (hence issues on Gojek, Grab, and WeChat). I wanted a better understanding of what makes Super Apps so powerful and what differentiates them from the monster FAANG apps of the west.

Gojek’s engineering blog provides the most succinct definition of a Super App,

“A Super App is many apps within an umbrella app. It’s an Operating System that unbundles the tyranny of apps. It’s a portal to the internet for a mobile-first generation”

While these days there are many Super Apps (and many companies trying to be Super Apps), the term Super App is most often associated with WeChat, the massively popular Chinese Super App. In the context of WeChat, you will often hear it described as the “one app to rule them all”

|  |

The “One Ring to Rule Them All” from Lord of the Rings

While WeChat may have been the first app to embody the principles of a modern SuperApp, the origin of the term dates back to 2010.

Does the name Mike Lazaridis mean anything to you? Mike is the founder of Research in Motion (“RIM”), manufacturer of the BlackBerry device. Mike is also the inventor of the concept of a Super App.

In 1999 BlackBerry debuted one of the world’s first smartphones, the BlackBerry 850.

|  |

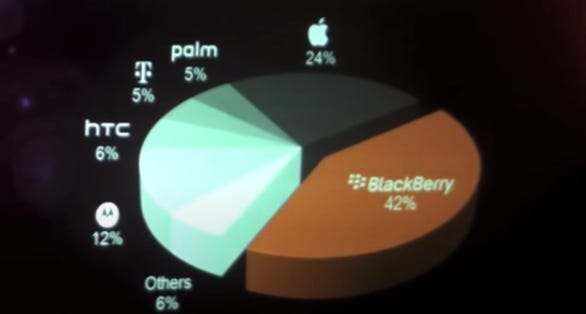

By 2010, the Blackberry was on top of the world

In 2010, about half of every smartphone shipped in the world was a BlackBerry device (see chart).

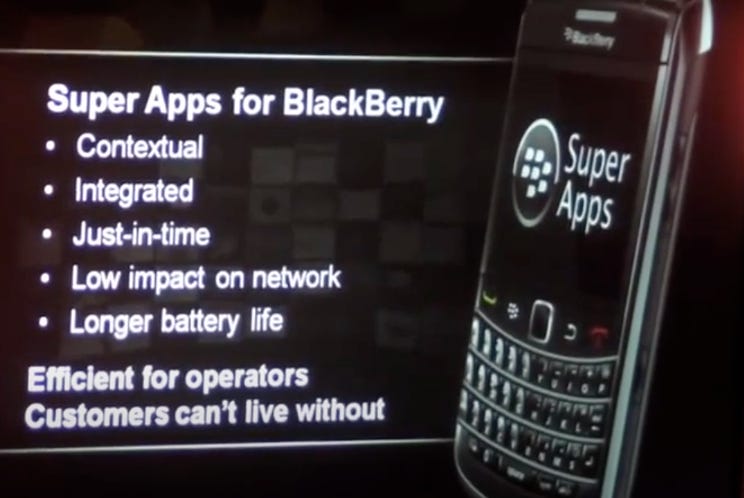

In a speech at Mobile World Congress 2010, Blackberry CEO, Mike Lazaridis introduced the concept of a Super App.

Mike defined Super Apps as:

“Super-apps are integrated with other apps, giving a seamless experience across the device. They’re contextual - aware of things like your location and status”

“SuperApps are apps that once you start using them, you wonder how you ever previously lived without them”

Or as Crackberry.com summarizes:

“Applications which make use of all the BlackBerry resources available. […] Deep integration across the whole device.”

(While these features sound common now, this speech was in 2010 so some of these things were impressive at the time.)

Mike was describing apps that could talk to each other. For example, he walks through a user looking at an eBay auction and then automatically syncing with the calendar so they could get a reminder when the auction is about to end.

Mike viewed this as a way to create lock-in for the Blackberry device. He was trying to demonstrate that only on Blackberry could you connect apps to each other, turning your calendar app or eBay app into a SuperApp with a seamless, integrated experience.

The core difference between Mike’s definition and the modern definitions is that Mike’s was hardware dependent. By using the Calendar app or eBay on a Blackberry, those apps would be ‘supercharged’.

The difference with modern Super Apps is that e.g., WeChat is hardware agnostic. In general, there aren’t notable differences between WeChat on Android and WeChat and iOS.

A modern Super App like Gojek could build their own smartphones to further integrate the Gojek experience into users’ lives, but Gojek likely views hardware as commoditized. Both Gojek and Grab’s early go-to-market strategies involved bulk buying cheap smartphones and giving them to drivers on installment plans because most of their drivers did not own smartphones. The markets that many Super Apps operate in (Indonesia, Malaysia, India, Thailand, etc.) don’t have a lot of purchasing power when it comes to smartphones.

Today, Blackberry devices are mostly a relic of history. While I give Mike and Blackberry credit for creating the term Super App, they can’t get credit for the value capture and ecosystem that modern Super Apps have built.

In the rest of this issue, we will cover:

(Side note: Surprisingly, Blackberry still did about $1bn in revenue last year, but that’s down from a peak in 2011 of about $20bn).

(Sources: Mike’s full Super App presentation on YouTube: Part 1, Part 2, Part 3)

Each Super App took a unique path to become one. There is no single set path to building a Super App (i.e., you don’t need messaging, you don’t need native ridesharing):

There are, however, several characteristics that each of the Super Apps I’ve studied have or are in the process of adding:

And one bonus characteristic:

Some potentially less obvious benefits:

If you live in America, you’ve heard of Super Apps. If you live in Asia, you’ve used one.

If you look at Europe and North America, there are no dominant Super Apps. It’s impossible to say with certainty why Super Apps aren’t common in western countries (and I’ll specifically talk about America here since it’s the country I’m most familiar with), but here are my four hypotheses:

1

It’s tough to build a Super App for a country with an established internet economy (e.g., America). The current group of well-known Super Apps started in countries with underdeveloped internet economies. WeChat (China — at the time was underdeveloped), Gojek (Indonesia), Grab (Malaysia and southeast Asia), Alipay (China), Zalo (Vietnam), Paytm (India), and others.

Part of this is due to the fact that there is already such a wide selection of apps in the United States that it would be tough for one app to consolidate all of those applications’ features into one (better!) “Super App” experience.

Some of this is due to path dependency. Talking about QR codes in China, Ben Thompson says,

It is tempting to look at how payments work in countries like China, but that ignores the path dependency of one market using cash until recently, and the other receiving unsolicited Bank Americards 51 years ago. Once a job is done — and credit cards do their jobs very well — it takes a 10x improvement to get users to switch, and, in a three-sided network, that 10x is 10

In the same way that the US and China are on different paths regarding payments, we’re also on different paths regarding applications and the mobile web.

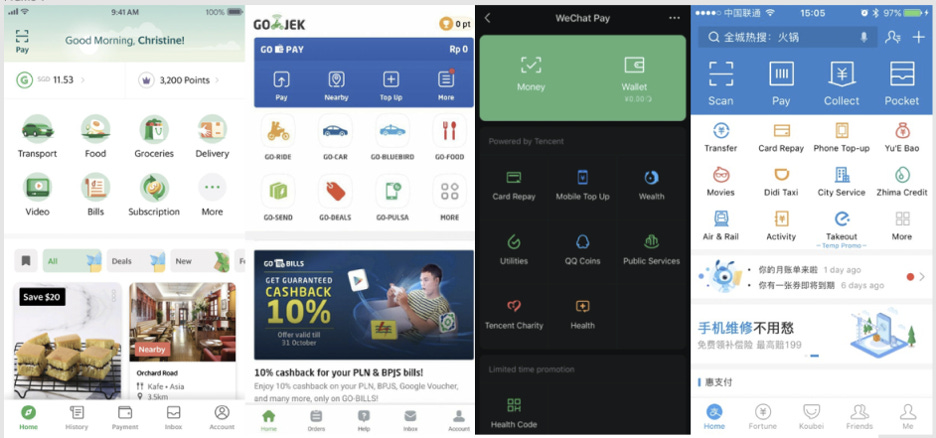

Super Apps could simplistically be thought of as platform companies that are able to build out many verticals within one app. This has worked well in markets like China, Indonesia, etc. because those markets did not have strong incumbent competitors.

After Gojek had a strong market position in ride-sharing, you could imagine a very MBA-like conversation happening at the company where leaders asked, “what is the next biggest TAM market that is underserved that we can cross-sell our existing user base?” From there they landed on markets like insurance, travel, medicine, and all the other many products they offer.

It’s possible that several app experiences within one app could be superior, but at this point, many in the west are okay with and have been trained to be okay switching between multiple apps for things, adding credit card info to new apps, and all the other laborious functions of adding new apps.

Uber, iMessage, and Twitter all do their individual jobs well. A new app that wants to recreate all those experiences would have a high bar to clear to get users to switch.

(h/t Abheek Anand for guiding my thinking here)

2

Super Apps are mobile experiences and most western countries are not mobile-first countries.

Even though Indonesian internet usage is surging, reaching about ~65% of the population in 2019, only about 26% of the population were using a computer as of 2018.

Super Apps are primed for their mobile experiences. As far as I know, Gojek and Grab don’t offer desktop experiences. WeChat notoriously has a very stripped down and basic desktop experience (basically, just chat).

As America becomes a more mobile-first country (with younger generations leading the charge), it’s possible we could see popular consumer apps (e.g., TikTok) add Super App like functionality.

On the individual app level, what are some new apps that have taken historically desktop-based experiences and turned them into mobile experiences for younger generations? This has been prevalent throughout the FinTech industry. There’s no better example than Robinhood turning your brokerage account into a sleek mobile experience. All the challenger/neo-banks fit these criteria of taking previously clunky, desktop experiences, and turning them into sleek mobile experiences.

3.

As I proposed in my earlier WeChat issue, “To be a truly generalizable Super App, you need to own your user’s wallet.”

A key element of all the Super Apps I’ve previously covered is that they own or have a direct connection to users’ bank accounts. Part of this is due to the fact that in the countries these apps operate, the populations were largely unbanked or cash-dependent prior to the Super App’s solution. To some degree, companies like Gojek needed to help their users move into digital payments because it made it easier for them to process transactions. Also, compare this to the US where only about 7% of the population is unbanked.

This explains why you see aspiring Super Apps like Facebook (via Facebook Financial) or Uber (via Uber Money) really trying to earn their user’s deposits. But again, the problem is that many Americans are pretty satisfied with their current bank/digital wallet offerings and so there will be a high bar to get them to switch to an alternative product.

When you own your users’ deposits, benefits include:

4.

It is important that Super Apps have strong positive relations with the governments of the countries they operate within. The leaders of countries with Super Apps, seem to really love them. The Indonesian President fired a cabinet member that appeared to be anti-Gojek and then appointed Gojek’s founder to his next cabinet. You can’t get much cozier than that. Well, unless you’re Tencent (WeChat’s owner). There are countless articles talking about censorship within WeChat at the behest of the Chinese government and I believe Tencent’s top executives are also official members of the CCP (as most top company execs must be in China).

In today’s political climate, it’s challenging to imagine an American or European leader going out of their way to promote a burgeoning Super App. Look at how western democracies have treated Facebook and Uber.

As we’ve covered in prior issues, Gojek and Grab have lots of pro-nationalist marketing in which they align themselves with the growth of the companies they operate in.

From Uber v. Gojek (Nationalist Marketing & Gov’t Relations):

Since early on, Gojek’s marketing language made strong nationalist appeals. As one example, the jackets for each country’s drivers have their national flags embroidered on them. They made an effort to align themselves with all of the countries that they operated in.

And that’s not all just marketing. Gojek appears to make meaningful contributions to Indonesia’s GDP and has increased the standard of living for its drivers. In the case of Grab, Malaysia notoriously had one of the most dangerous taxi industries in the world. While I haven’t seen exact measurements, it’s possible they’ve also increased foreigner’s willingness to visit the country (good for tourism, small businesses, taxes, etc.).

In the case of WeChat, you could argue that the Chinese government likes most of the country’s online activity taking place within one centralized ecosystem where all of someone’s transactions and conversations are linked.

The second point related to government relations is that the US and Europe have stricter anti-trust laws than the rest of the world. If American leaders are talking about breaking up Facebook, OH BOY would they hate an app with dominance and reach like WeChat. Given both the stricter regulation in the west and the current political climate towards big tech, it is possible that regulation could be the biggest barrier to entry of a Super App ever reaching a level of influence like WeChat commands.

As I’m writing this post (September 4, 2020), the Justice Department of the USA is reportedly planning to file an antitrust case against Google

Riffing off the hypotheses from above, it’s possible that a Super App could bloom here as the US becomes more mobile-centric due to gen-z and younger generations.

Anecdotally, I (a millennial) remember desperately wanting a Mac in middle school. My 17-year old sister (Gen-Z) could care less about what computer she has (she happily uses the free Chromebook her school gives her).

While I believe it will be difficult for a Western-focused company to build a generalizable Super App (this won’t stop them from trying!), I do believe it is possible for entrepreneurs and existing companies within western markets to build powerful Super Apps for X.

Some examples of this include

There are a number of western apps already trying to brand themselves as a Super App.

Within the finance category, here are a few examples:

(Source)

Speaking about Revolut, another commentator said:

“Revolut has become an expert at shipping new products and features (loyalty, share trading, currency conversion and so on), and is now very much considered to be in the ‘super app’ category. Could they become the WeChat of the UK?”

My reaction:

Now, you might be reading this and saying, isn’t a “Super App for X” just a “vertically-integrated app”. Well, yes and no.

The difference between a Super App and a vertically integrated app is that a Super app is open and allows other companies to live within its ecosystem, acting as a marketplace or portal, whereas a vertically integrated app is the owner or developer of all the apps within its ecosystem

In my Gojek article I called this out saying:

“When building a SuperApp (one app for many things) that integrates dozens of services you can opt to build services in-house, have third-party APIs where people can build their own apps, or have formal partnerships where you integrate another company’s services into your app. […] In mid-2018, Gojek launched its third-party platform (“TPP”) so that businesses besides Gojek could build apps on its platform. Their goal was to turn Gojek into the operating system of the phone. WeChat enjoys this luxury in China and Gojek wanted the same relationship with Indonesians and other Southeast Asian citizens. Gojek, seems to have relied more on developing services in-house than other SuperApps and this was their chance to begin branching out.”

From Aditi Sharma, Grab’s Director and Head of Startup Programs & Investments:

“It is clear from the beginning that doing this all by ourselves is not entirely practical. Strategically it makes more sense for us to build a healthy ecosystem of partners around our users. “Hence we are constantly seeking quality partners in the ecosystem to work with on our everyday superapp vision,”

The evolution from a regular app to a Super App looks something like this:

By this definition, only WeChat is a full Super App. Grab and Gojek are still on step 2, while many of the aspiring Western Super Apps are still on step 1.

For example, let’s take M1 Finance, a Chicago, USA-based company. They do offer several functions (checking account with a debit card, borrowing, investing), but all of those functions are created, managed, and offered by M1.

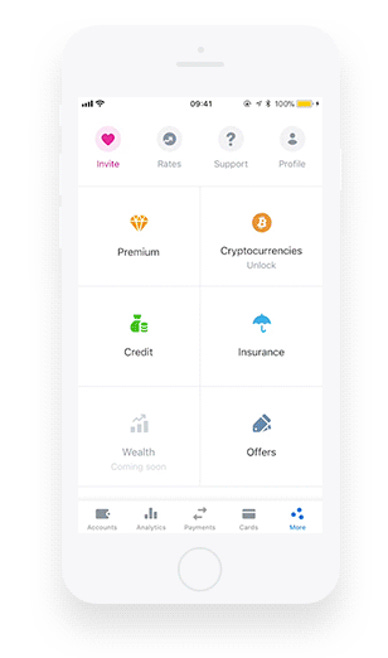

Let’s take a deeper look at Revolut. Going through their offerings, they include things such as: checking accounts, money transfers, stock and cryptocurrency purchasing, insurance, and other financial related transactions. While some of these might look like partnerships (Stock trading via DriveWealth, Insurance via Simplesurance), they are not in the same way that WeChat and Didi or Gojek and Halodoc are partners.

Revolut uses DriveWealth to provide stock trading and uses Simplesurance for their insurance products, but DriveWealth and Simplesurance are behind-the-scenes service providers. Most people trading stocks with Revolut will have no idea they are trading with DriveWealth as a third-party broker.

This is different than if Revolut users could click on “trading” in the Revolut app and it took them to a Robinhood or E-Trade UI that was built into Revolut.

(Above is a photo of one of the Revolut UIs. Look familiar? 🤔🤔🤔🤔)

The Super App craze has swept eastern countries and western entrepreneurs want to build Super Apps of their own, but many of them are struggling to embrace the open nature of building a Super App. For many reasons, I predict we will see more apps trying to brand themselves as Super Apps because, not least of which, branding yourself a Super App leads to a higher valuation than “vertically integrated” does😉

I’m excited to see attempts at building more Super Apps and I’m eager to try out American contenders.

In my next issue, I will go through the crop of aspiring Super Apps (Facebook, Uber, WhatsApp, Amazon, and more!) and break down the bull and bear case for each of them with ideas of my own.

Until then, thanks for reading! If you enjoyed this issue, please share it on Twitter, Hacker News, Reddit, or wherever people might enjoy it!

Something fun to end on. If you’ve ever been to a nightclub in China, you’ve certainly heard “Made in China” by the Higher Brothers. Check our their other song, “WeChat”.

Thanks for reading💜,

Ryan Rodenbaugh, @ryanrodenbaugh

First published on September 6, 2020